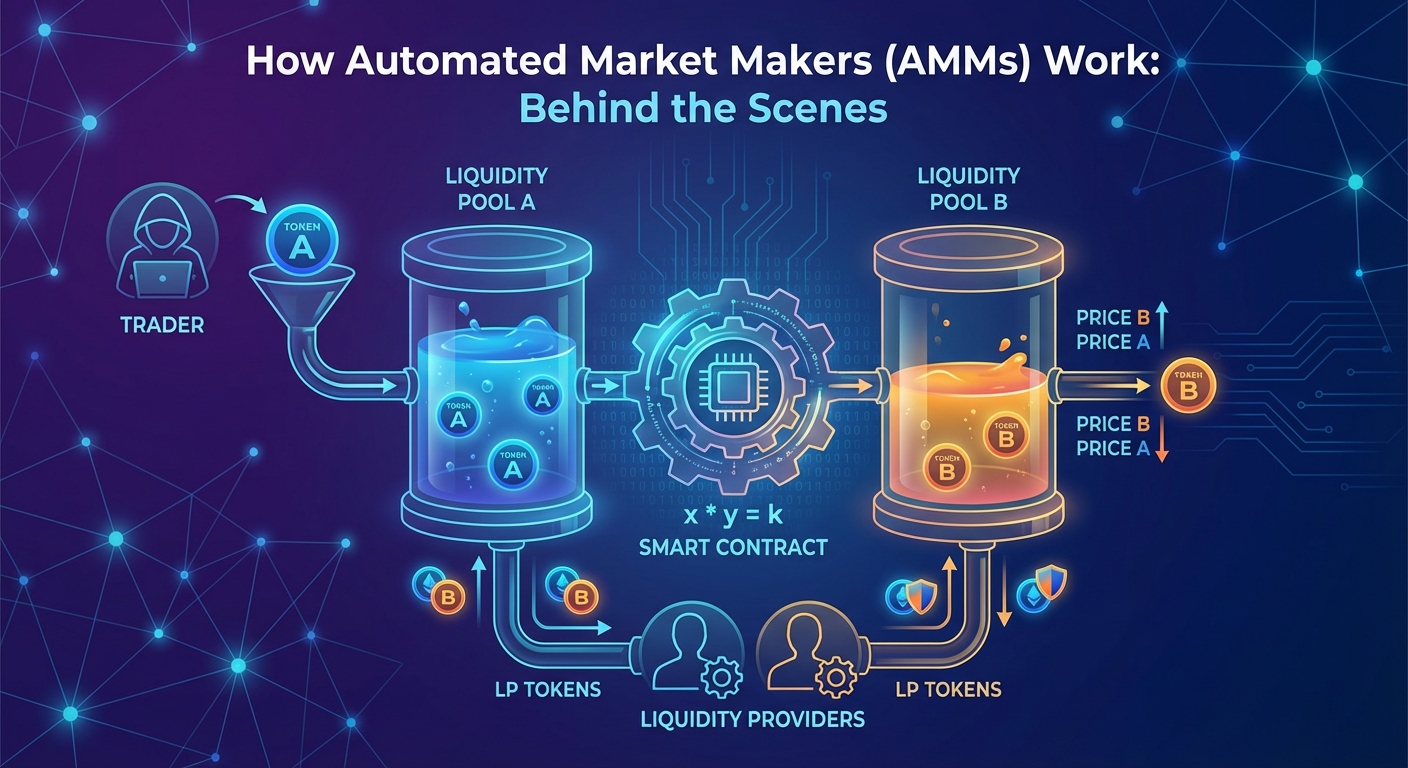

Traditional exchanges rely on order books where buyers and sellers place bids and asks. Automated market makers flip that model entirely. Instead of matching individual orders, they use liquidity pools and mathematical formulas to determine prices automatically. No human intermediaries. No waiting for a counterparty. Just code executing trades 24/7.

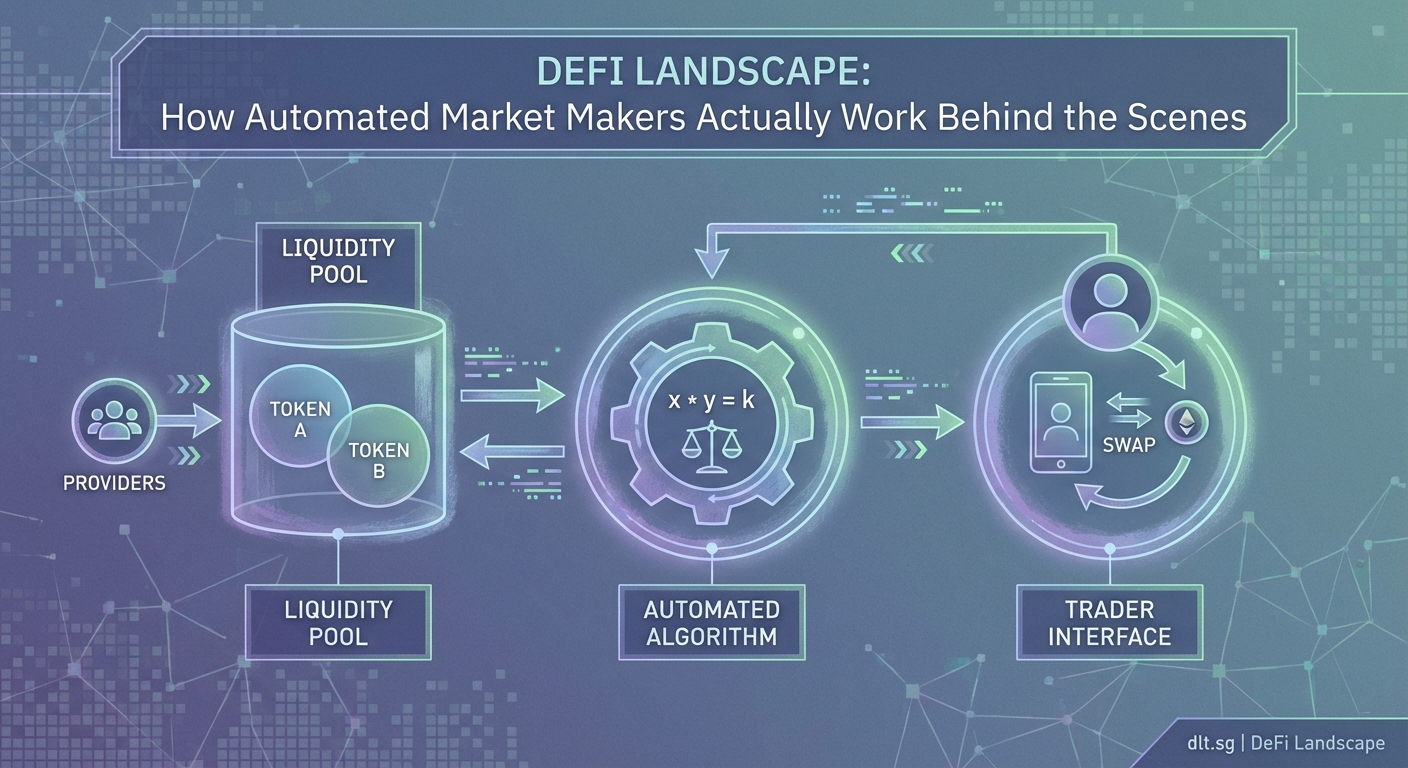

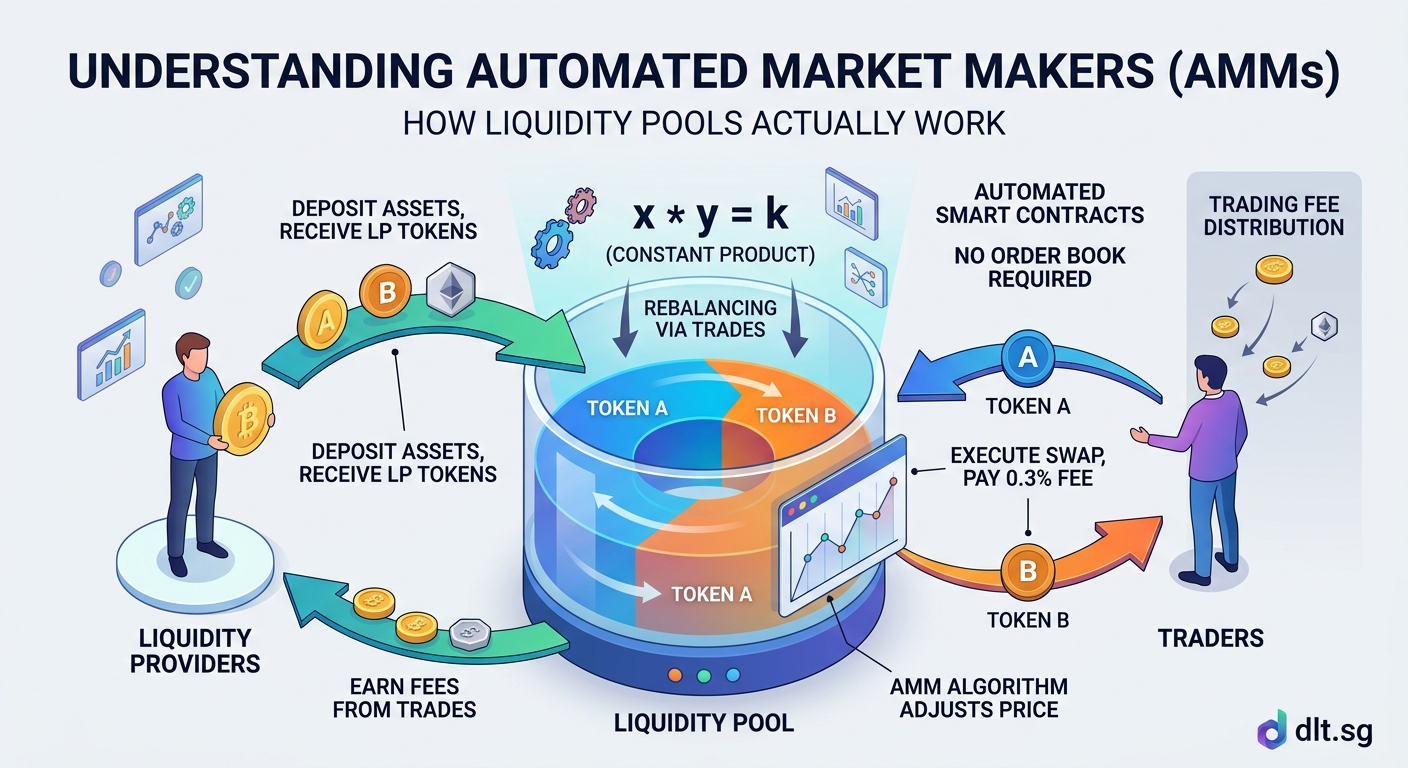

Automated market makers use liquidity pools funded by providers who deposit token pairs. Smart contracts apply pricing formulas like the constant product model to calculate exchange rates. When you trade, the contract adjusts pool ratios and updates prices algorithmically. This system enables permissionless, decentralized trading without traditional order books or centralized intermediaries controlling asset custody.

What makes automated market makers different from traditional exchanges

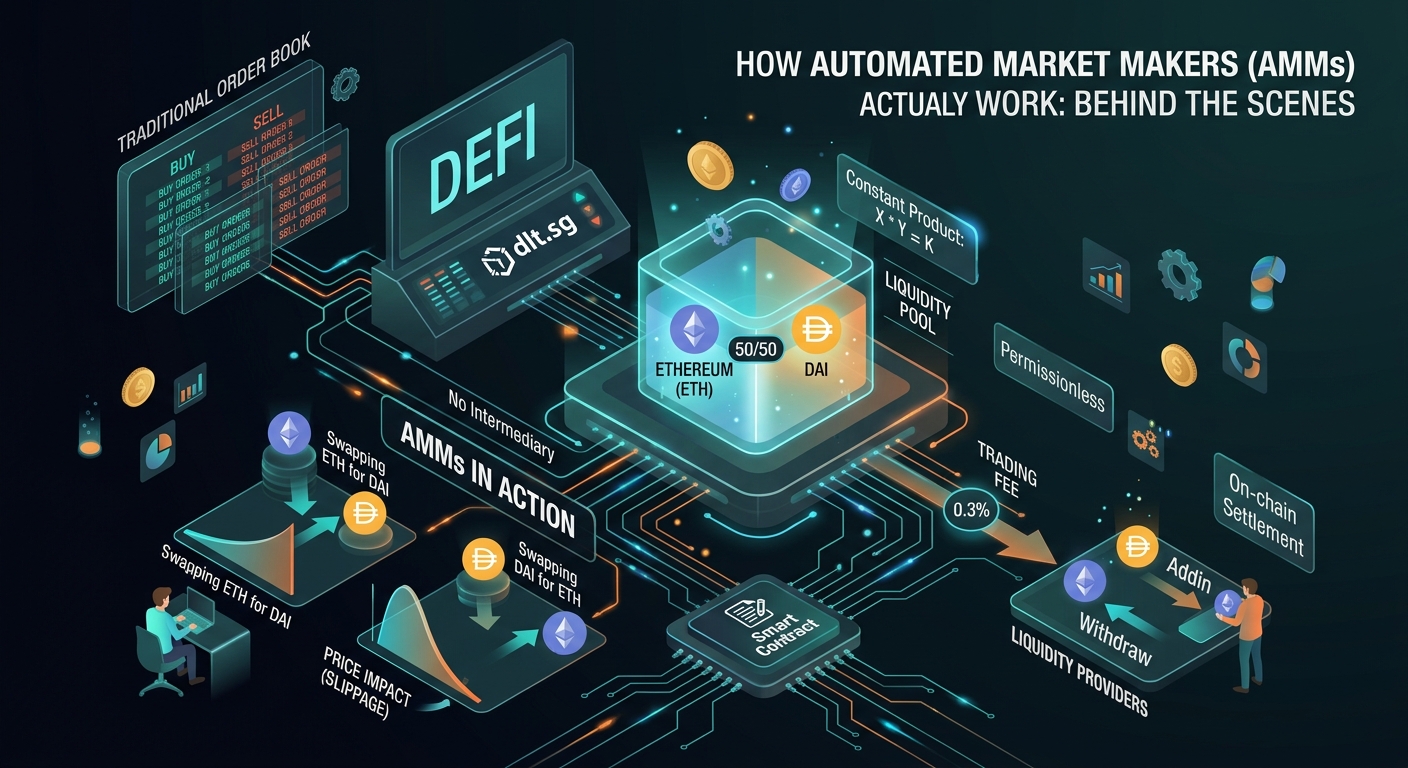

Centralized exchanges like Binance or Coinbase maintain order books. You submit a limit order at $2,000 for one ETH. The exchange stores that order until someone agrees to sell at your price.

Automated market makers skip the order book entirely. They pool liquidity from multiple providers into a single smart contract. When you want to swap ETH for USDC, the contract calculates the price based on the ratio of tokens already in the pool. No matching engine. No waiting for a seller.

The contract holds all assets. You interact directly with the protocol, not a company holding your funds. That architectural shift removes custodial risk and censorship vectors.

How distributed ledgers actually work explains the foundation that makes these trustless pools possible.

The anatomy of a liquidity pool

A liquidity pool is a smart contract holding two tokens. Picture a vault with ETH on one side and USDC on the other. Liquidity providers deposit equal values of both tokens to earn fees from traders.

If the pool holds 10 ETH and 20,000 USDC, the implied price is 2,000 USDC per ETH. The contract maintains a mathematical relationship between the two quantities.

When you trade, you deposit one token and withdraw the other. The contract recalculates the ratio and updates the price accordingly. The larger the trade relative to pool size, the more the price shifts.

Pools need sufficient depth to minimize slippage. A pool with 1,000 ETH and 2 million USDC can handle bigger trades without dramatic price swings compared to a pool with 10 ETH and 20,000 USDC.

The constant product formula explained

Most automated market makers use the constant product formula: x * y = k. Here, x represents the quantity of token A, y represents the quantity of token B, and k is a constant that never changes.

Let’s use real numbers. A pool holds 100 ETH and 200,000 USDC. Multiply them: 100 * 200,000 = 20,000,000. That’s your constant k.

You want to buy 10 ETH. You’ll remove 10 ETH from the pool, leaving 90 ETH. To keep k constant, the USDC quantity must adjust. Solve for the new USDC amount: 90 * y = 20,000,000. That gives y = 222,222 USDC.

The pool started with 200,000 USDC. Now it has 222,222 USDC. You deposited 22,222 USDC to get 10 ETH. Your effective price was 2,222 USDC per ETH, higher than the initial 2,000 USDC per ETH because your trade shifted the ratio.

The formula ensures the pool never runs out of either token. As one side depletes, the price rises exponentially, making further purchases prohibitively expensive.

Step by step: executing a swap on an AMM

Here’s what happens when you swap tokens on an automated market maker:

- You connect your wallet to the decentralized exchange interface and specify the trade (e.g., swap 1 ETH for USDC).

- The interface queries the smart contract to calculate how much USDC you’ll receive based on current pool reserves.

- You review the quoted price, estimated slippage, and transaction fee, then approve the swap.

- Your wallet signs the transaction and broadcasts it to the network.

- The smart contract debits 1 ETH from your wallet and credits it to the liquidity pool.

- The contract recalculates the pool ratio using the pricing formula and determines the USDC output.

- The contract transfers the calculated USDC amount to your wallet.

- Liquidity providers earn a small percentage of your trade as a fee, proportional to their share of the pool.

What happens when you send a blockchain transaction breaks down the underlying mechanics of steps four through seven.

Why liquidity providers participate

Liquidity providers deposit tokens into pools to earn trading fees. Every swap generates a small fee, typically 0.3%, which accumulates in the pool. Providers receive fees proportional to their share of total liquidity.

If you contribute 5% of a pool’s liquidity, you earn 5% of all trading fees. High-volume pools generate substantial fee income. A pool processing $10 million in daily volume at 0.3% fees generates $30,000 daily, split among all providers.

Providers receive liquidity pool tokens representing their share. These tokens are fungible and transferable. You can withdraw your liquidity anytime by redeeming your LP tokens for the underlying assets.

The system incentivizes users to supply liquidity where it’s most needed. Pools with insufficient liquidity suffer high slippage, making them unattractive to traders. That creates opportunities for providers willing to supply capital.

Common AMM variations and their trade-offs

| AMM Type | Formula | Best For | Limitations |

|---|---|---|---|

| Constant Product | x * y = k | General purpose trading | High slippage for large trades |

| Constant Sum | x + y = k | Stable asset pairs | Liquidity can be fully drained |

| Hybrid (Curve) | Combines product and sum | Stablecoin swaps | Complex to implement |

| Concentrated Liquidity | Custom price ranges | Capital efficiency | Requires active management |

Constant product models work well for volatile pairs like ETH/USDC because they maintain liquidity across all price ranges. The formula prevents the pool from emptying completely.

Constant sum models suit stablecoins trading near 1:1 ratios. They minimize slippage for trades where prices shouldn’t deviate much. But they risk total depletion if prices diverge significantly.

Curve Finance pioneered hybrid models that behave like constant sum near the current price but shift toward constant product at extremes. This reduces slippage for stablecoin swaps while maintaining safety.

Concentrated liquidity lets providers specify price ranges where their capital operates. This boosts capital efficiency but requires monitoring and rebalancing as prices move.

The impermanent loss problem

Liquidity providers face a subtle risk called impermanent loss. It occurs when token prices diverge from their ratio at deposit time.

Suppose you deposit 1 ETH and 2,000 USDC when ETH trades at $2,000. The pool’s total value is $4,000 from your contribution. If ETH rises to $4,000, arbitrageurs will trade USDC for ETH until the pool reflects the new price.

The constant product formula means the pool will rebalance to roughly 0.707 ETH and 2,828 USDC (0.707 * 2,828 ≈ 2,000, maintaining k). Your share is now worth about $5,656 (0.707 ETH * $4,000 + $2,828 USDC).

But if you’d simply held 1 ETH and 2,000 USDC without providing liquidity, you’d have $6,000 (1 ETH * $4,000 + $2,000 USDC). You lost $344 to impermanent loss.

The loss is “impermanent” because it disappears if prices return to the original ratio. But if you withdraw while prices have diverged, the loss becomes permanent.

Impermanent loss is the price you pay for earning trading fees. Calculate whether fee income over your holding period exceeds potential losses from price divergence. Volatile pairs magnify this risk, while stable pairs minimize it.

Price oracles and arbitrage in AMM ecosystems

Automated market makers don’t fetch external price data. They derive prices purely from pool ratios. This creates arbitrage opportunities when AMM prices diverge from broader market rates.

If ETH trades at $2,000 on centralized exchanges but an AMM pool implies $1,950, arbitrageurs will buy ETH from the pool and sell it elsewhere. This activity pushes the AMM price back toward market rates.

Arbitrage is how AMMs stay synchronized with external markets. The constant product formula means any deviation creates a profit opportunity that incentivizes correction.

Some protocols integrate price oracles to improve capital efficiency or enable features like lending. But core AMM functionality operates without external data feeds, relying instead on economic incentives to maintain accurate pricing.

Gas costs and transaction mechanics

Every AMM interaction requires gas to execute smart contract functions. Swapping tokens on Ethereum mainnet can cost $5 to $50 depending on network congestion. Complex operations like adding liquidity to multiple pools cost more.

Layer 2 solutions like Arbitrum and Optimism reduce gas costs by processing transactions off the main chain while inheriting Ethereum’s security. AMM swaps on these networks often cost under $1.

Understanding blockchain nodes covers how different node types validate these transactions across network layers.

Gas costs eat into profits for small trades and frequent rebalancing. Consider transaction fees when calculating expected returns from liquidity provision. A $100 trade paying $10 in gas loses 10% before accounting for slippage or fees.

Security considerations for AMM users

Smart contract bugs pose the biggest risk to AMM users. A flaw in the contract code could allow attackers to drain liquidity pools. Major protocols undergo extensive audits, but vulnerabilities still emerge.

Reentrancy attacks let malicious contracts repeatedly withdraw funds before the pool updates its balance. Flash loan attacks manipulate pool ratios to extract value. Oracle manipulation can trick protocols relying on external price feeds.

Stick to established protocols with proven track records and multiple audits. Check if the protocol has bug bounties and insurance funds to cover losses. Review the contract’s permissions to ensure developers can’t arbitrarily modify pool parameters.

Front-running is another concern. Bots monitor pending transactions and submit competing trades with higher gas fees to execute first. This can worsen your slippage or prevent your transaction from completing at your expected price.

Advanced AMM features and innovations

Modern AMMs incorporate features beyond basic token swaps. Multi-asset pools hold three or more tokens, enabling complex rebalancing strategies. Weighted pools let liquidity providers adjust token ratios (e.g., 80% ETH, 20% USDC) to maintain specific exposures.

Dynamic fees adjust based on market volatility. During calm periods, fees decrease to attract volume. During volatility, fees increase to compensate providers for elevated impermanent loss risk.

Just-in-time liquidity provision lets sophisticated actors add liquidity right before large trades execute, capture fees, then immediately withdraw. This maximizes fee income while minimizing impermanent loss exposure.

Some protocols implement loss mitigation mechanisms. Single-sided liquidity provision lets users deposit one token instead of pairs. The protocol automatically manages the other side using treasury funds or specialized strategies.

Comparing AMMs to traditional market making

Traditional market makers are firms or individuals who continuously quote buy and sell prices. They profit from the bid-ask spread while providing liquidity. This requires significant capital, market access, and sophisticated algorithms.

Automated market makers democratize this function. Anyone with tokens can provide liquidity and earn fees. No special permissions or relationships required. The smart contract handles all pricing and execution logic.

Traditional makers actively manage inventory and adjust quotes based on market conditions. AMMs passively follow their programmed formulas. This simplicity enables permissionless participation but reduces adaptability to market dynamics.

Order book exchanges offer price-time priority. The first order at a given price executes first. AMMs execute all trades at the current algorithmic price regardless of submission order (though network-level ordering still matters for front-running).

Real-world AMM adoption and volume

Uniswap processes billions in weekly trading volume across thousands of token pairs. Curve dominates stablecoin swaps with over $100 billion in total value locked at peak adoption. PancakeSwap leads on BNB Chain with similarly massive volumes.

What Singapore banks are actually doing with blockchain technology explores how traditional finance is beginning to adopt AMM concepts for digital asset trading.

Institutional players now use AMMs for large over-the-counter trades. Protocols like CoW Swap batch multiple trades together to improve pricing and reduce gas costs. This makes AMMs viable for professional trading desks managing substantial capital.

The growth reflects AMMs solving real problems: 24/7 trading, permissionless access, no custody risk, and transparent pricing. These advantages outweigh limitations like impermanent loss and slippage for many use cases.

Regulatory considerations for AMM participation

Regulatory treatment of automated market makers varies globally. Some jurisdictions classify liquidity provision as securities activity requiring registration. Others treat it as peer-to-peer exchange falling outside traditional frameworks.

Are your DeFi protocols compliant? Understanding Singapore’s stance on decentralized finance examines the local regulatory landscape.

Tax implications depend on your jurisdiction. Many tax authorities treat each swap as a taxable event. Liquidity providers may owe taxes on fee income and impermanent loss/gain upon withdrawal. Tracking basis and calculating gains across multiple pools becomes complex.

Know-your-customer requirements increasingly apply to DeFi protocols, especially those with centralized components like frontend hosting or token governance. Some protocols implement geo-blocking or identity verification to comply with local regulations.

Practical tips for getting started with AMMs

Start small while learning the mechanics. Deposit a modest amount into an established pool like ETH/USDC on Uniswap. Monitor how fees accumulate and how price movements affect your position value.

Calculate your break-even point. Estimate daily fee income based on pool volume and your share. Determine how long you need to provide liquidity for fees to exceed potential impermanent loss at various price scenarios.

Consider your risk tolerance and time horizon. Volatile pairs offer higher fee potential but greater impermanent loss risk. Stable pairs generate lower fees but minimize loss risk. Match your choice to your goals.

Track your positions using portfolio management tools. Many services aggregate data across protocols, showing current value, fee earnings, and impermanent loss in real time. This visibility helps you make informed decisions about when to withdraw or rebalance.

Here are common mistakes to avoid:

- Providing liquidity to low-volume pools that don’t generate enough fees to justify risk

- Ignoring gas costs when calculating expected returns from small positions

- Failing to account for impermanent loss when comparing AMM returns to simple holding

- Using unaudited protocols or pools with suspicious token contracts

- Providing liquidity to highly volatile pairs without understanding downside scenarios

Making AMMs work for your DeFi strategy

Automated market makers represent a fundamental shift in how decentralized markets operate. They replace centralized intermediaries with transparent, algorithmic systems anyone can access.

The constant product formula and liquidity pool model enable permissionless trading without order books. Liquidity providers earn fees for supplying capital. Traders get instant execution without counterparty risk.

Understanding how these systems work behind the scenes helps you make better decisions. You can evaluate whether providing liquidity makes sense for your situation. You can estimate potential returns and risks more accurately. You can choose appropriate pools and protocols based on your goals.

The technology continues evolving. New AMM designs improve capital efficiency, reduce impermanent loss, and enable more complex trading strategies. Staying informed about these developments positions you to take advantage of opportunities as they emerge.

Start experimenting with small amounts. Watch how prices update as trades execute. Track your fee earnings and position value over time. The hands-on experience will deepen your understanding far more than theory alone.